题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[单选题]

An 8% $30 million convertible loan note was issued on 1 April 20X5 at par. Interest is

A.$5,976,000

B.$1,524,000

C.$324,000

D.$9,000,000

提问人:网友陈珊

发布时间:2022-01-07

题目内容

(请给出正确答案)

A.$5,976,000

B.$1,524,000

C.$324,000

D.$9,000,000

更多“An 8% $30 million convertible …”相关的问题

更多“An 8% $30 million convertible …”相关的问题

group mainly operates a chain of national restaurants and provides vending and other catering services to corporate

clients. All restaurants offer ‘eat-in’, ‘take-away’ and ‘home delivery’ services. The draft consolidated financial

statements for the year ended 30 September 2005 show revenue of $42·2 million (2004 – $41·8 million), profit

before taxation of $1·8 million (2004 – $2·2 million) and total assets of $30·7 million (2004 – $23·4 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In September 2005 the management board announced plans to cease offering ‘home delivery’ services from the

end of the month. These sales amounted to $0·6 million for the year to 30 September 2005 (2004 – $0·8

million). A provision of $0·2 million has been made as at 30 September 2005 for the compensation of redundant

employees (mainly drivers). Delivery vehicles have been classified as non-current assets held for sale as at 30

September 2005 and measured at fair value less costs to sell, $0·8 million (carrying amount,

$0·5 million). (8 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

A.$5,976,000

B.$1,524,000

C.$324,000

D.$9,000,000

,

, ,欲完成两个多项式相加、相乘和相除

,欲完成两个多项式相加、相乘和相除 的运算,则以下哪个程序正确?

的运算,则以下哪个程序正确?

A.a= [1 0 6 2]; b= [2 6 8]; C=a+b D=conv(a,b) [q,r]=deconv(a,b)

B.a= [1 0 6 2]; b= [2 6 8]; C=a+(0,b) D=conv(a,b) [q,r]=deconv(a,b)

C.a= [1 6 2]; b= [2 6 8]; C=a+b D=conv(a,b) [q,r]=deconv(a,b)

D.a= [1 0 6 2]; b= [2 6 8]; C=a+b D=conv(a,b) E=deconv(a,b)

,,欲完成两个多项式相加、相乘和相除的运算,则以下哪个程序正确?

A.a= [1 0 6 2]; b= [2 6 8]; C=a+b D=conv(a,b) [q,r]=deconv(a,b)

B.a= [1 0 6 2]; b= [2 6 8]; C=a+[0,b] D=conv(a,b) [q,r]=deconv(a,b)

C.a= [1 6 2]; b= [2 6 8]; C=a+b D=conv(a,b) [q,r]=deconv(a,b)

D.a= [1 0 6 2]; b= [2 6 8]; C=a+b D=conv(a,b) E=deconv(a,b)

Property at cost (useful life 15 years) $45 million

Accumulated depreciation $6 million

On 1 April 2014, Dune decided to sell the property. The property is being marketed by a property agent at a price of $42 million, which was considered a reasonably achievable price at that date. The expected costs to sell have been agreed at $1 million. Recent market transactions suggest that actual selling prices achieved for this type of property in the current market conditions are 10% less than the price at which they are marketed.At 30 September 2014 the property has not been sold.

At what amount should the property be reported in Dune’s statement of financial position as at 30 September 2014?

A、$36 million

B、$37·5 million

C、$36·8 million

D、$42 million

(a) IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors contains guidance on the use of accounting policies and accounting estimates.

Required:

Explain the basis on which the management of an entity must select its accounting policies and distinguish, with an example, between changes in accounting policies and changes in accounting estimates. (5 marks)

(b) The directors of Tunshill are disappointed by the draft profi t for the year ended 30 September 2010. The company’s assistant accountant has suggested two areas where she believes the reported profi t may be improved:

(i) A major item of plant that cost $20 million to purchase and install on 1 October 2007 is being depreciated on a straight-line basis over a fi ve-year period (assuming no residual value). The plant is wearing well and at the beginning of the current year (1 October 2009) the production manager believed that the plant was likely to last eight years in total (i.e. from the date of its purchase). The assistant accountant has calculated that, based on an eight-year life (and no residual value) the accumulated depreciation of the plant at 30 September 2010 would be $7·5 million ($20 million/8 years x 3). In the fi nancial statements for the year ended 30 September 2009, the accumulated depreciation was $8 million ($20 million/5 years x 2). Therefore, by adopting an eight-year life, Tunshill can avoid a depreciation charge in the current year and instead credit $0·5 million ($8 million – $7·5 million) to the income statement in the current year to improve the reported profi t. (5 marks)

(ii) Most of Tunshill’s competitors value their inventory using the average cost (AVCO) basis, whereas Tunshill uses the fi rst in fi rst out (FIFO) basis. The value of Tunshill’s inventory at 30 September 2010 (on the FIFO basis) is $20 million, however on the AVCO basis it would be valued at $18 million. By adopting the same method (AVCO) as its competitors, the assistant accountant says the company would improve its profi t for the year ended 30 September 2010 by $2 million. Tunshill’s inventory at 30 September 2009 was reported as $15 million, however on the AVCO basis it would have been reported as $13·4 million. (5 marks)

Required:

Comment on the acceptability of the assistant accountant’s suggestions and quantify how they would affect the fi nancial statements if they were implemented under IFRS. Ignore taxation.

Note: the mark allocation is shown against each of the two items above.

A、$32,000

B、$40,000

C、$46,000

D、$60,000

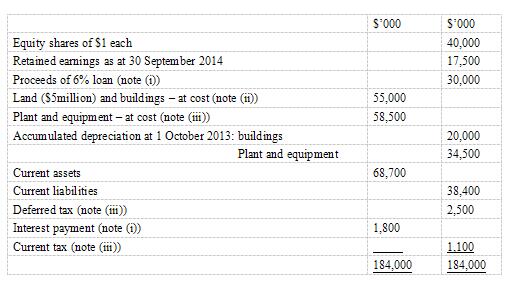

s for the year ended 30 September 2014 and adding the year’s profit (before any adjustments required by notes (i) to (iii) below) to retained earnings, Kandy as at 30 September 2014 is:

The following notes are relevant:

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(ii)Non-current assets: The price of property has increased significantly in recent years and on 1 October 2013, the directors decided to revalue the land and buildings. The directors accepted the report of an independent surveyor who valued the land at $8 million and the buildings at $39 million on that date. The remaining life of the buildings at 1 October 2013 was 15 years. Kandy does not make an annual transfer to retained profits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate of Kandy is 20%.

Plant and equipment is depreciated at 121⁄2% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current asset for the year ended 30 September 2014.

(iii)A provision of $2·4 million is required for current income tax on the profit of the year to 30 September 2014. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), Kandy has further taxable temporary differences of $10 million as at 30 September 2014.

Required:

(a) Prepare a schedule of adjustments required to the retained earnings of Kandy as at 30 September 2014 as a result of the information in notes (i) to (iii) above.

(b) Prepare the statement of financial position of Kandy as at 30 September 2014.

What is the total provision (extraction plus dismantling) which Xplorer would report in its statement of financial position as at 30 September 2014 in respect of its oil operations().

A、$34,900,000

B、$24,532,000

C、$22,900,000

D、$4,132,000

A、7.5

B、8

C、7

D、6.5

(b) Seymour offers health-related information services through a wholly-owned subsidiary, Aragon Co. Goodwill of

$1·8 million recognised on the purchase of Aragon in October 2004 is not amortised but included at cost in the

consolidated balance sheet. At 30 September 2006 Seymour’s investment in Aragon is shown at cost,

$4·5 million, in its separate financial statements.

Aragon’s draft financial statements for the year ended 30 September 2006 show a loss before taxation of

$0·6 million (2005 – $0·5 million loss) and total assets of $4·9 million (2005 – $5·7 million). The notes to

Aragon’s financial statements disclose that they have been prepared on a going concern basis that assumes that

Seymour will continue to provide financial support. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Seymour Co for the year ended

30 September 2006.

NOTE: The mark allocation is shown against each of the three issues.

为了保护您的账号安全,请在“简答题”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!

微信搜一搜

微信搜一搜

简答题

微信搜一搜

简答题

简答题

微信搜一搜

简答题

如搜索结果不匹配,请

如搜索结果不匹配,请