题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[主观题]

In the process of conjugation, the genes of Hfr strain enter into F- strain in a certain linear order. The closer the gene is to the origin of transfer, the earlier it enters into F- cell.

提问人:网友hcbaa1988

发布时间:2022-01-07

题目内容

(请给出正确答案)

更多“In the process of conjugation,…”相关的问题

更多“In the process of conjugation,…”相关的问题

A、1,000

B、2,000

C、1,100

D、1,200

1) Milling is carried out on a machine tool called a “milling machine” that is used for the shaping of metal and other solid materials. 2) Casting is a manufacturing process by which a liquid material is poured into a mold containing a cavity of the desired shape, and then allowed to solidify. 3) Stamping is a metal working process in which sheet metal is formed into a desired shape by pressing or punching it on a machine press. 4) With current technology, the most effective method of CO ₂ capture from the flue gas of a PC plant is by chemical reaction with an organic solvent such as monoethanolamine (MEA), one of a family of amine compounds. In a vessel called an absorber, the flue gas is “scrubbed” with an amine solution, typically capturing 85% to 90% of the CO ₂. The CO ₂ -laden solvent is then pumped to a second vessel, called a regenerator, where heat is applied (in the form of steam) to release the CO ₂. The resulting stream of concentrated CO ₂ is then compressed and piped to a storage site, while the depleted solvent is recycled back to the absorber.

LG Co is in the process of setting standard costs for next period. Product F uses two types of material, M and N. 6 kg of material M and 5 kg of material N are to be used, at a standard price of $2 per kg and $3 per kg respectively. Three hours of skilled labour and one hour of semi-skilled labour will be required for each unit of F. Wage rates will be $8 per hour and $6 per hour respectively. Production overhead is to be absorbed at a rate of $4 per labour hour. Ten per cent is to be added to total production cost to absorb administration, selling and distribution costs. The standard cost of production for one unit of F will be:

A、$57.00

B、$69.00

C、$73.00

D、$80.30

Due to the failure to settle the debts due, Jianshe Garment Trading Co Ltd (Jianshe Co) was declared bankrupt by its creditors. In October 2010 the court rendered an order to accept the application of bankruptcy and designated a bankruptcy administrator. During the process of bankruptcy liquidation the bankruptcy administrator found that Jianshe Co had given up a credit of RMB 200,000 yuan owed by its affiliate enterprise in August 2009.

The bankruptcy administrator also found that some shareholders of Jianshe Co failed to made full capital contributions as prescribed in the agreement of incorporation.

Required:

Answer the following questions in accordance with the Enterprise Bankruptcy Law of China, and give your reasons for your answer:

(a) (i) State whether the action of giving up credit can be revoked during the process of liquidation; (4 marks)

(ii) State whether the court should grant an order to revoke the act of giving up credit. (3 marks)

(b) State how to deal with the matter of the lack of full capital contributions by some of the shareholders of Jianshe Co. (3 marks)

(i) Hangle Garment Co had given up a credit of RMB 500,000 yuan owed by its affiliate enterprise in August 2013;

(ii) Some shareholders of Hangle Garment Co failed to make full capital contributions as prescribed in the articles of association of the company;

(iii) There was a contract between Hangle Garment Co and Bright Department Store, which was concluded before the bankruptcy application was accepted and had been partly performed.

Required:

In accordance with the Enterprise Bankruptcy Law of China:

(a) State whether the action of giving up credit could be revoked during the process of liquidation. (2 marks)

(b) State how the lack of full capital contributions by some of the shareholders of the company should be dealt with. (2 marks)

(c) State what right the bankruptcy administrator has regarding the partly-performed contract between Hangle Garment Co and Bright Department Store. (2 marks)

(c) In April 2006, Keffler was banned by the local government from emptying waste water into a river because the

water did not meet minimum standards of cleanliness. Keffler has made a provision of $0·9 million for the

technological upgrading of its water purifying process and included $45,000 for the penalties imposed in ‘other

provisions’. (5 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Keffler Co for the year ended

31 March 2006.

NOTE: The mark allocation is shown against each of the three issues.

Bronze operate several chemical processing factories across the country, it manufactures 24 hours a day, seven days a week and employees work a standard shift of eight hours and are paid for hours worked at an hourly rate. Factory employees are paid weekly, with approximately 80% being paid by bank transfer and 20% in cash; the different payment methods are due to employee preferences and Bronze has no plans to change these methods. The administration and sales teams are paid monthly by bank transfer.

Factory staff are each issued a sequentially numbered clock card which details their employee number and name. Employees swipe their cards at the beginning and end of the eight-hour shift and this process is not supervised. During the shift employees are entitled to a 30-minute paid break and employees do not need to clock out to access the dining area. Clock card data links into the payroll system, which automatically calculates gross and net pay along with any statutory deductions. The payroll supervisor for each payment run checks on a sample basis some of these calculations to ensure the system is operating effectively.

Bronze has a human resources department which is responsible for setting up new permanent employees and leavers. Appointments of temporary staff are made by factory production supervisors. Occasionally overtime is required of factory staff, usually to fill gaps caused by staff holidays. Overtime reports which detail the amount of overtime worked are sent out quarterly by the payroll department to production supervisors for their review.

To encourage staff to attend work on time for all shifts Bronze pays a discretionary bonus every six months to factory staff; the production supervisors determine the amounts to be paid. This is communicated in writing by the production supervisors to the payroll department and the bonus is input by a clerk into the system.

For employees paid by bank transfer, the payroll manager reviews the list of the payments and agrees to the payroll records prior to authorising the bank payment. If any changes are required, the payroll manager amends the records. For employees paid in cash, the pay packets are prepared in the payroll department and a clerk distributes them to employees; as she knows most of these individuals she does not require proof of identity.

Required:

(a) Identify and explain FIVE internal control STRENGTHS in Bronze Industries Co’s payroll system. (5 marks)

(b) Identify and explain SIX internal control DEFICIENCIES in Bronze Industries Co’s payroll system and provide a RECOMMENDATION to address each of these deficiencies. (12 marks)

(c) Describe substantive ANALYTICAL PROCEDURES you should perform. to confirm Bronze Industries Co’s payroll expense. (3 marks)

Pear International Co (Pear) is a manufacturer of electrical equipment. It has factories across the country and its customer base includes retailers as well as individuals, to whom direct sales are made through their website. The company’s year end is 30 September 2012. You are an audit supervisor of Apple & Co and are currently reviewing documentation of Pear’s internal control in preparation for the interim audit.

Pear’s website allows individuals to order goods directly, and full payment is taken in advance. Currently the website is not integrated into the inventory system and inventory levels are not checked at the time when orders are placed.

Goods are despatched via local couriers; however, they do not always record customer signatures as proof that the customer has received the goods. Over the past 12 months there have been customer complaints about the delay between sales orders and receipt of goods. Pear has investigated these and found that, in each case, the sales order had been entered into the sales system correctly but was not forwarded to the despatch department for fulfilling.

Pear’s retail customers undergo credit checks prior to being accepted and credit limits are set accordingly by sales ledger clerks. These customers place their orders through one of the sales team, who decides on sales discount levels.

Raw materials used in the manufacturing process are purchased from a wide range of suppliers. As a result of staff changes in the purchase ledger department, supplier statement reconciliations are no longer performed. Additionally, changes to supplier details in the purchase ledger master file can be undertaken by purchase ledger clerks as well as supervisors.

In the past six months Pear has changed part of its manufacturing process and as a result some new equipment has been purchased, however, there are considerable levels of plant and equipment which are now surplus to requirement. Purchase requisitions for all new equipment have been authorised by production supervisors and little has been done to reduce the surplus of old equipment.

Required:

(a) In respect of the internal control of Pear International Co:

(i) Identify and explain FIVE deficiencies;

(ii) Recommend a control to address each of these deficiencies; and

(iii) Describe a test of control Apple & Co would perform. to assess if each of these controls is operating effectively. (15 marks)

(b) Describe substantive procedures you should perform. at the year end to confirm each of the following for plant and equipment:

(i) Additions; and

(ii) Disposals. (4 marks)

(c) Pear’s finance director has expressed an interest in Apple & Co performing other review engagements in addition to the external audit; however, he is unsure how much assurance would be gained via these engagements and how this differs to the assurance provided by an external audit.

Required:

Identify and explain the level of assurance provided by an external audit and other review engagements. (3 marks)

Pear’s directors are considering establishing an internal audit department next year, and the finance director has asked about the differences between internal audit and external audit and what impact, if any, establishing an internal audit department would have on future external audits performed by Apple & Co.

Required:

(d) Distinguish between internal audit and external audit. (4 marks)

(e) Explain the potential impact on the work performed by Apple & Co during the interim and final audits, if Pear International Co was to establish an internal audit department. (4 marks)

(i) Revaluation of property, plant and equipment (PPE)

At the beginning of the year, management undertook an extensive review of Elounda Co’s non-current asset valuations and as a result decided to update the carrying value of all PPE. The finance director, Peter Dullman, contacted his brother, Martin, who is a valuer and requested that Martin’s firm undertake the valuation, which took place in August 20X5. (5 marks)

(ii) Inventory valuation

Your firm attended the year-end inventory count for Elounda Co and ascertained that the process for recording work in progress (WIP) and finished goods was acceptable. Both WIP and finished goods are material to the financial statements and the quantity and stage of completion of all ongoing production was recorded accurately during the count.

During the inventory count, the count supervisor noted that a consignment of finished goods, compound E243, with a value of $720,000, was defective in that the chemical mix was incorrect. The finance director believes that compound E243 can still be sold at a discounted sum of $400,000. (6 marks)

(iii) Bank loan

Elounda Co secured a bank loan of $2·6 million on 1 October 20X4. Repayments of $200,000 are due quarterly, with a lump sum of $800,000 due for repayment in January 20X7. The company met all loan payments in 20X5 on time, but was late in paying the April and July 20X6 repayments. (4 marks)

Required:

(a) Describe substantive procedures you should perform. to obtain sufficient, appropriate audit evidence in relation to the above three matters.

Note: The mark allocation is shown against each of the three matters above.

(b) Describe the procedures which the auditor of Elounda Co should perform. in assessing whether or not the company is a going concern. (5 marks)

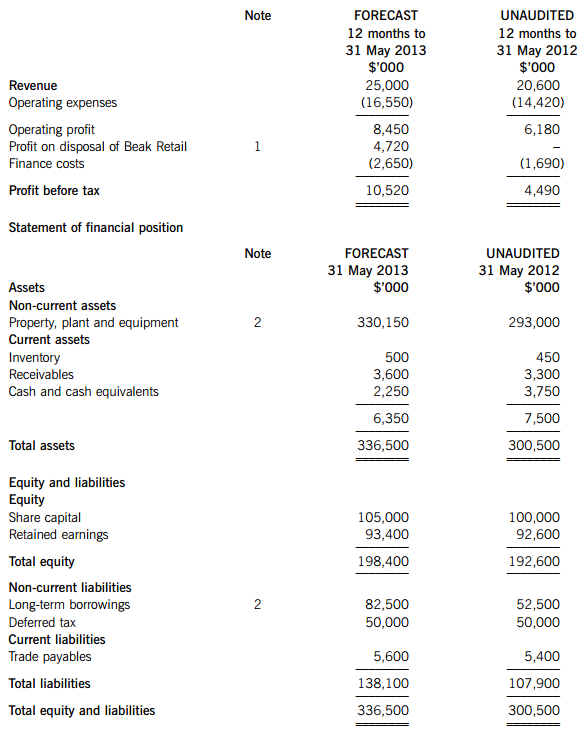

(a) You are a manager in Lapwing & Co. One of your audit clients is Hawk Co which operates commercial real estate properties typically comprising several floors of retail units and leisure facilities such as cinemas and health clubs, which are rented out to provide rental income.

Your firm has just been approached to provide an additional engagement for Hawk Co, to review and provide a report on the company’s business plan, including forecast financial statements for the 12-month period to 31 May 2013. Hawk Co is in the process of negotiating a new bank loan of $30 million and the report on the business plan is at the request of the bank. It is anticipated that the loan would be advanced in August 2012 and would carry an interest rate of 4%. The report would be provided by your firm’s business advisory department and a second partner review will be conducted which will reduce any threat to objectivity to an acceptable level.

Extracts from the forecast financial statements included in the business plan are given below:

Statement of comprehensive income (extract)

Notes:

1. Beak Retail is a retail park which is underperforming. Its sale is currently being negotiated, and is expected to take place in September 2012.

2. Hawk Co is planning to invest the cash raised from the bank loan in a new retail and leisure park which is being developed jointly with another company, Kestrel Co.

Required:

In respect of the engagement to provide a report on Hawk Co’s business plan:

(i) Identify and explain the matters that should be considered in agreeing the terms of the engagement; and Note: You are NOT required to consider ethical threats to objectivity. (6 marks)

(ii) Recommend the procedures that should be performed in order to examine and report on the forecast financial statements of Hawk Co for the year to 31 May 2013. (13 marks)

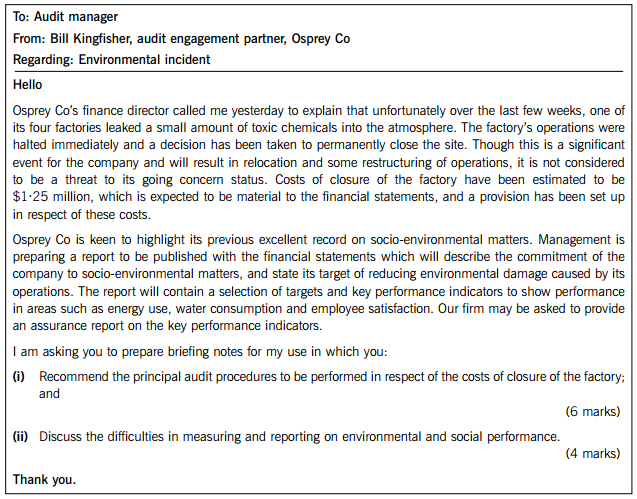

(b) You are also responsible for the audit of Osprey Co, which has a financial year ended 31 May 2012. The audit engagement partner, Bill Kingfisher, sent you the following email this morning:

Required:

Respond to the partner’s email. (10 marks)

Note: the split of the mark allocation is shown within the partner’s email.

Professional marks will be awarded in part (b) for the presentation and clarity of your answer. (4 marks)

(a) Auditors have a responsibility under ISA 265 Communicating Deficiencies in Internal Control to those Charged with Governance and Management, to communicate deficiencies in internal controls. In particular SIGNIFICANT deficiencies in internal controls must be communicated in writing to those charged with governance.

Required:

Explain examples of matters the auditor should consider in determining whether a deficiency in internal controls is significant. (5 marks)

Greystone Co is a retailer of ladies clothing and accessories. It operates in many countries around the world and has expanded steadily from its base in Europe. Its main market is aimed at 15 to 35 year olds and its prices are mid to low range. The company’s year end was 30 September 2010.

In the past the company has bulk ordered its clothing and accessories twice a year. However, if their goods failed to meet the key fashion trends then this resulted in significant inventory write downs. As a result of this the company has recently introduced a just in time ordering system. The fashion buyers make an assessment nine months in advance as to what the key trends are likely to be, these goods are sourced from their suppliers but only limited numbers are initially ordered.

Greystone Co has an internal audit department but at present their only role is to perform. regular inventory counts at the stores.

Ordering process

Each country has a purchasing manager who decides on the initial inventory levels for each store, this is not done in conjunction with store or sales managers. These quantities are communicated to the central buying department at the head office in Europe. An ordering clerk amalgamates all country orders by specified regions of countries, such as Central Europe and North America, and passes them to the purchasing director to review and authorise.

As the goods are sold, it is the store manager’s responsibility to re-order the goods through the purchasing manager; they are prompted weekly to review inventory levels as although the goods are just in time, it can still take up to four weeks for goods to be received in store.

It is not possible to order goods from other branches of stores as all ordering must be undertaken through the purchasing manager. If a customer requests an item of clothing, which is unavailable in a particular store, then the customer is provided with other branch telephone numbers or recommended to try the company website.

Goods received and Invoicing

To speed up the ordering to receipt of goods cycle, the goods are delivered directly from the suppliers to the individual stores. On receipt of goods the quantities received are checked by a sales assistant against the supplier’s delivery note, and then the assistant produces a goods received note (GRN). This is done at quiet times of the day so as to maximise sales. The checked GRNs are sent to head office for matching with purchase invoices.

As purchase invoices are received they are manually matched to GRNs from the stores, this can be a very time consuming process as some suppliers may have delivered to over 500 stores. Once the invoice has been agreed then it is sent to the purchasing director for authorisation. It is at this stage that the invoice is entered onto the purchase ledger.

Required:

(b) As the external auditors of Greystone Co, write a report to management in respect of the purchasing system which:

(i) Identifies and explains FOUR deficiencies in that system;

(ii) Explains the possible implication of each deficiency;

(iii) Provides a recommendation to address each deficiency.

A covering letter is required.

Note: Up to two marks will be awarded within this requirement for presentation. (14 marks)

(c) Describe substantive procedures the auditor should perform. on the year-end trade payables of Greystone Co. (5 marks)

(d) Describe additional assignments that the internal audit department of Greystone Co could be asked to perform. by those charged with governance. (6 marks)

为了保护您的账号安全,请在“简答题”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!

微信搜一搜

微信搜一搜

简答题

微信搜一搜

简答题

简答题

微信搜一搜

简答题

如搜索结果不匹配,请

如搜索结果不匹配,请