题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[主观题]

(iii) the warranty provision. (3 marks)

(iii) the warranty provision. (3 marks)

提问人:网友hyg1978

发布时间:2022-01-06

题目内容

(请给出正确答案)

(iii) the warranty provision. (3 marks)

更多“(iii) the warranty provision. …”相关的问题

更多“(iii) the warranty provision. …”相关的问题

A—purchase confirmation B—cable confirmation

C—advice of arrival D—circular letter of credit

E—check register F—advice of bill collected

G—after-sales warranty H—agency bills

I—advice note J—affidavit of means

K—affidavit of service L—advice of bill accepted

M—advice of drawing N—agency receipt

O—advice of bill paid P—advice of authority to pay

Q—advice of settlement

51. ()电报确认书 ()汇票通知书

52. ()授权付款通知书 ()巡回信用证

53. ()支票登记簿 ()代理票据

54. ()送达证时书 ()票据付款通知书

55. ()到货通知 ()票据收款通知书

A.P波时限0.10s

B.P波电压肢导0.25mV

C.II、III、aVF导联直立,aVR导联倒置

D.P-R间期O.12S

E.II、III、aVF导联倒置,aVR导联直立

(1) 给出事件A、B的例子,使得

(i) P(A|B)<P(A),(ii) P(A|B)=P(A),(iii) P(A|B)>P(A).

(2) 设事件A,B,C相互独立,证明(i)C与AB相互独立.(ii) C与A∪B相互独立.

(3) 设事件A的概率P(A)=0,证明对于任意另一事件B,有A,B相互独立.

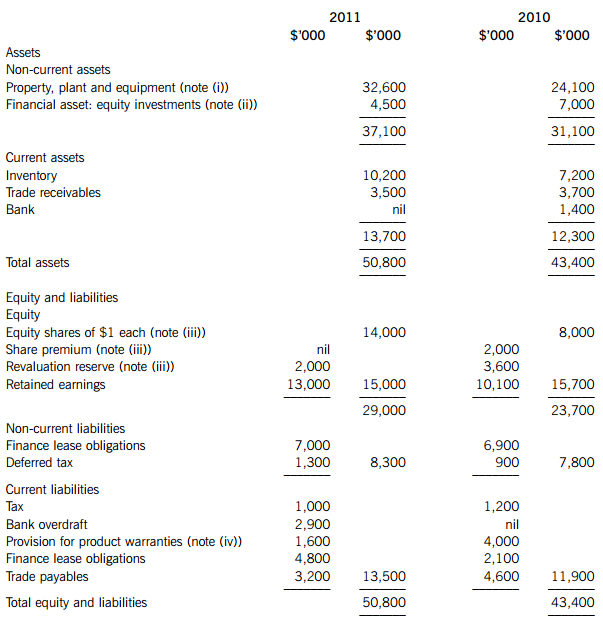

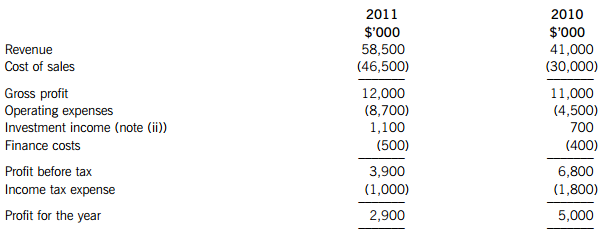

(a) The following information relates to the draft financial statements of Mocha.

Summarised statements of financial position as at 30 September:

Summarised income statements for the years ended 30 September:

The following additional information is available:

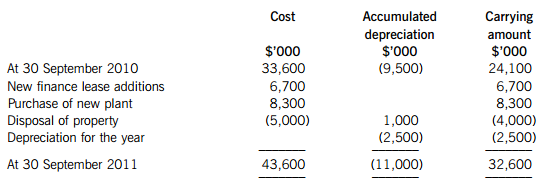

(i) Property, plant and equipment:

The property disposed of was sold for $8·1 million.

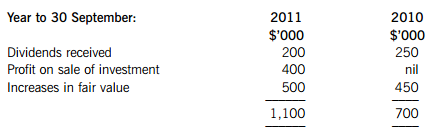

(ii) Investments/investment income:

During the year an investment that had a carrying amount of $3 million was sold for $3·4 million. No investments were purchased during the year.

Investment income consists of:

(iii) On 1 April 2011 there was a bonus issue of shares that was funded from the share premium and some of the revaluation reserve. This was followed on 30 April 2011 by an issue of shares for cash at par.

(iv) The movement in the product warranty provision has been included in cost of sales.

Required:

Prepare a statement of cash flows for Mocha for the year ended 30 September 2011, in accordance with IAS 7 Statement of cash flows, using the indirect method. (19 marks)

(b) Shareholders can often be confused when trying to evaluate the information provided to them by a company’s financial statements, particularly when comparing accruals-based information in the income statement and the statement of financial position with that in the statement of cash flows.

Required: In the two areas stated below, illustrate, by reference to the information in the question and your answer to (a), how information in a statement of cash flows may give a different perspective of events than that given by accruals-based financial statements:

(i) operating performance; and

(ii) investment in property, plant and equipment.

The following mark allocation is provided as guidance for this requirement:

(i) 3 marks

(ii) 3 marks

为了保护您的账号安全,请在“简答题”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!

微信搜一搜

微信搜一搜

简答题

微信搜一搜

简答题

简答题

微信搜一搜

简答题

如搜索结果不匹配,请

如搜索结果不匹配,请