题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[主观题]

(ii) The shares held in Date Inc and the dividend income received from that company. (7 ma

(ii) The shares held in Date Inc and the dividend income received from that company. (7 marks)

提问人:网友cdly7475

发布时间:2022-01-06

题目内容

(请给出正确答案)

(ii) The shares held in Date Inc and the dividend income received from that company. (7 marks)

更多“(ii) The shares held in Date I…”相关的问题

更多“(ii) The shares held in Date I…”相关的问题

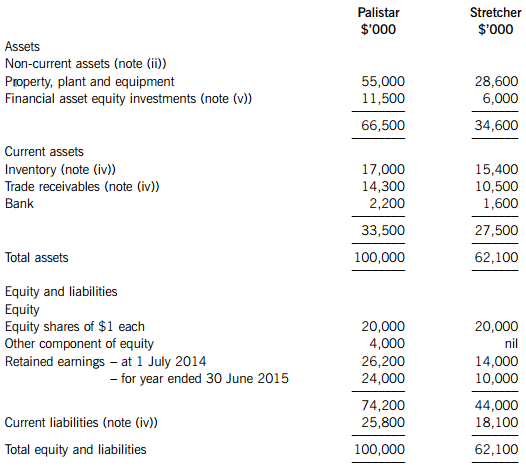

(a) On 1 January 2015, Palistar acquired 75% of Stretcher’s equity shares by means of an immediate share exchange of two shares in Palistar for five shares in Stretcher. The fair value of Palistar and Stretcher’s shares on 1 January 2015 were $4·00 and $3·00 respectively. In addition to the share exchange, Palistar will make a cash payment of $1·32 per acquired share, deferred until 1 January 2016. Palistar has not recorded any of the consideration for Stretcher in its financial statements. Palistar’s cost of capital is 10% per annum.

The summarised statements of financial position of the two companies as at 30 June 2015 are:

The following information is relevant:

(i) Stretcher’s business is seasonal and 60% of its annual profit is made in the period 1 January to 30 June each year.

(ii) At the date of acquisition, the fair value of Stretcher’s net assets was equal to their carrying amounts with the following exceptions:

An item of plant had a fair value of $2 million below its carrying value. At the date of acquisition it had a remaining life of two years.

The fair value of Stretcher’s investments was $7 million (see also note (v)).

Stretcher owned the rights to a popular mobile (cell) phone game. At the date of acquisition, a specialist valuer estimated that the rights were worth $12 million and had an estimated remaining life of five years.

(iii) Following an impairment review, consolidated goodwill is to be written down by $3 million as at 30 June 2015.

(iv) Palistar sells goods to Stretcher at cost plus 30%. Stretcher had $1·8 million of goods in its inventory at 30 June 2015 which had been supplied by Palistar. In addition, on 28 June 2015, Palistar processed the sale of $800,000 of goods to Stretcher, which Stretcher did not account for until their receipt on 2 July 2015. The in-transit reconciliation should be achieved by assuming the transaction had been recorded in the books of Stretcher before the year end. At 30 June 2015, Palistar had a trade receivable balance of $2·4 million due from Stretcher which differed to the equivalent balance in Stretcher’s books due to the sale made on 28 June 2015.

(v) At 30 June 2015, the fair values of the financial asset equity investments of Palistar and Stretcher were $13·2 million and $7·9 million respectively.

(vi) Palistar’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose Stretcher’s share price at that date is representative of the fair value of the shares held by the non-controlling interest.

Required:

Prepare the consolidated statement of financial position for Palistar as at 30 June 2015. (25 marks)

(b) For many years, Dilemma has owned 35% of the voting shares and held a seat on the board of Myno which has given Dilemma significant influence over Myno. The other shares (65%) in Myno were held by many other shareholders who all owned less than 10% of the share capital. On this basis, Dilemma considered Myno to be an associate and has used equity accounting to account for its investment.

In March 2015, Agresso made an offer to buy all of the shares of Myno. The offer was supported by the majority of Myno’s directors. Dilemma did not accept the offer and held on to its shares in Myno.

On 1 April 2015, Agresso announced that it had acquired the other 65% of the share capital of Myno and immediately convened a board meeting at which three of the previous directors of Myno were replaced, including the seat held by Dilemma.

Required:

Explain how the investment in Myno should be treated in the consolidated statement of profit or loss of Dilemma for the year ended 30 June 2015 and the consolidated statement of financial position at 30 June 2015. (5 marks)

A、market value of all securities held divided by the number of shares outstanding (所持全部证券的市值除以流通股数)

B、book value of all assets held divided by the number of shares outstanding (持有的全部资产的账面价值除以流通股数)

C、future value of all assets held divided by the number of shares outstanding (持有的全部资产的未来价值除以流通股数)

D、book value of all securities held divided by the number of shares outstanding (所持全部证券的账面价值除以流通股数)

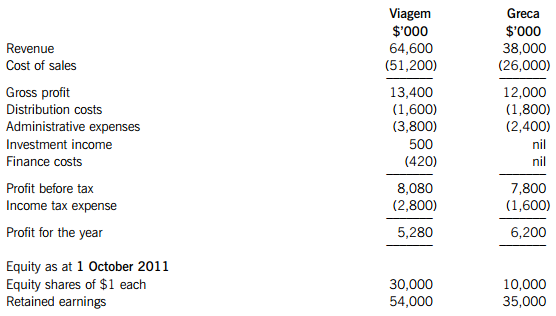

At the date of acquisition, shares in Viagem and Greca had a stock market value of $6·50 and $2·50 each, respectively.

Income statements for the year ended 30 September 2012

The following information is relevant:

(i) At the date of acquisition, the fair values of Greca’s assets were equal to their carrying amounts with the exception of two items:

– An item of plant had a fair value of $1·8 million above its carrying amount. The remaining life of the plant at the date of acquisition was three years. Depreciation is charged to cost of sales.

– Greca had a contingent liability which Viagem estimated to have a fair value of $450,000. This has not changed as at 30 September 2012.

Greca has not incorporated these fair value changes into its financial statements.

(ii) Viagem’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose, Greca’s share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest.

(iii) Sales from Viagem to Greca throughout the year ended 30 September 2012 had consistently been $800,000 per month. Viagem made a mark-up on cost of 25% on these sales. Greca had $1·5 million of these goods in inventory as at 30 September 2012.

(iv) Viagem’s investment income is a dividend received from its investment in a 40% owned associate which it has held for several years. The underlying earnings for the associate for the year ended 30 September 2012 were $2 million.

(v) Although Greca has been profitable since its acquisition by Viagem, the market for Greca’s products has been badly hit in recent months and Viagem has calculated that the goodwill has been impaired by $2 million as at 30 September 2012.

Required:

(a) Calculate the consolidated goodwill at the date of acquisition of Greca.

(b) Prepare the consolidated income statement for Viagem for the year ended 30 September 2012. The following mark allocation is provided as guidance for these requirements:

(a) 7 marks

(b) 14 marks

(c) The carrying amount of a subsidiary’s leased property will be subject to review as part of the fair value exercise on acquisition and may be subject to review in subsequent periods.

Required:

Explain how a fair value increase of a subsidiary’s leased property on acquisition should be treated in the consolidated financial statements; and how any subsequent increase in the carrying amount of the leased property might be treated in the consolidated financial statements.

Note: Ignore taxation. (4 marks)

A、A、 Shares being held by the directors of the Company cannot be transferred within three years after resignation.

B、B、 The company repurchases back 10 million of its shares within one year as stock options.

C、C、 Shares being held by Supervisor of the Company can be sold after being approved by the general shareholders meeting at the time of resignation.

D、D、 In any time, a company must not accept its own shares as collateral.

英译中

The "shareholders" as such had no knowledge of the lives, thoughts or needs of the workmen employed by the company in which he held shares, and his influence on the relations of capital and labor was not good.

A Co. Ltd.holdsa general shareholders meeting six months after it is incorporated. Which of the following the resolutions being adopted by the general meeting of shareholders compliance with the law? A、 Shares being held by Directors, supervisors and senior management of the company can be sold at any time. B、 Shares being held by promoters of the Company can be soldfrom today. C、 Company would purchase 4% of its sharesfor rewarding employees of the Company innext one year. D、 It decidesto operatereal estate jointly with Company B, and asksguarantee by its sharesbeing held by Company B forperforming the contract.

A、A. the ownership of the companies is open to the public

B、B. the shares of the companies cannot be purchased or sold by any member of the public.

C、C. the periodic financial reports of the companies are required by law.

D、D. the stocks and shares of the companies are freely traded on a stock exchange or in over the counter markets.

A.One month

B.Three months

C.Six months

D.Twelve months

The company A and B intend to raise a CO. LTD. They are allowed to offering to social, and which of the following implement behavior is against the law? A、 Subscription in record: the subscribers shall not be withdrawn once the Subscription Shares. B、 Conclude an underwriting agreement with a bank for selling shares and deposit of share proceeds, money from the sale of shares and the bank for deposit of share. C、 On the prospectus to inform: the articles of association of the subscribers will made jointly when found in the General Assembly D、 On the prospectus to inform: after the founding fully subscribed, establishment meeting would be held within 60 days.

Preemptive right is the stockholder's right______.

A.to participate in management by voting on matters that come before the stockholders

B.to receive a proportionate part of any dividend

C.to maintain one's proportionate ownership in the corporation

D.to receive a proportionate share (based on number of shares held ) of any assets remaining after the corporation pays its liabilities in liquidation

为了保护您的账号安全,请在“简答题”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!

微信搜一搜

微信搜一搜

简答题

微信搜一搜

简答题

简答题

微信搜一搜

简答题

如搜索结果不匹配,请

如搜索结果不匹配,请